The United States Stock Market has historically been dominated by institutional investors. Historically 90% of trades and orders in the market were from Banks, Pension Funds, Insurance Companies etc.

However, that percent has slowly been declining as retail investors, like you and I are placing more and more orders. With the advent of commission-free trades, regular people are realizing that the market is an accessible way to make some money.

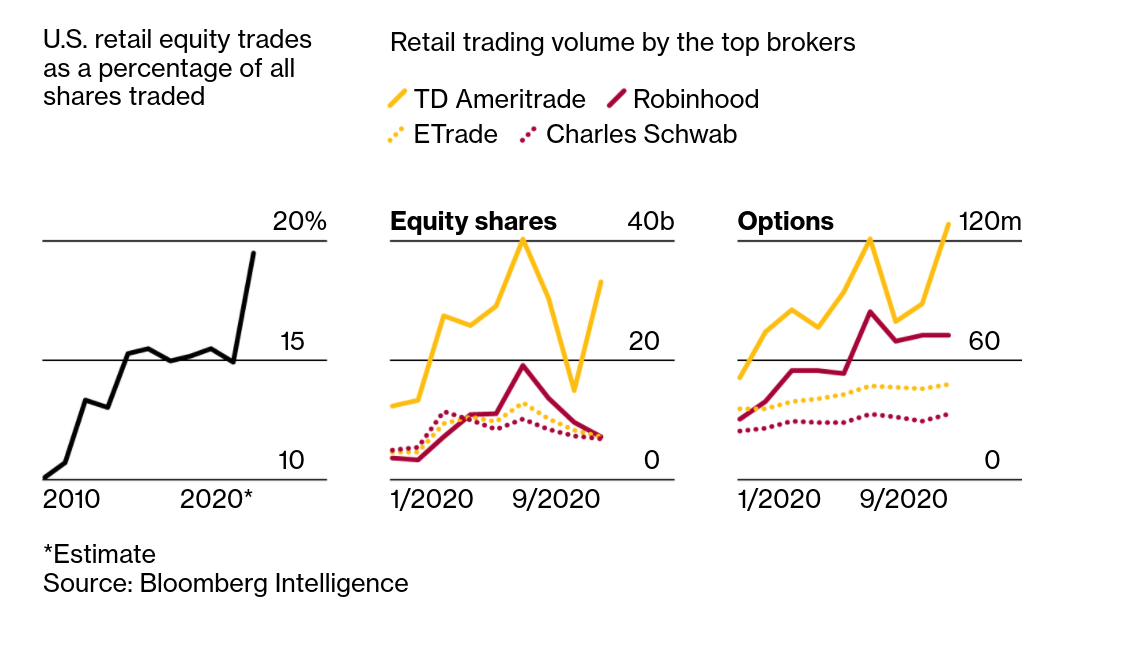

Recently, however, with the spread of COVID-19 and people staying at home, we've seen a huge surge in the number of trades (order flow) from Retail Investors. This is likely because people are finding more time, that used to be spent commuting and travelling, to invest (gamble ;) ) in the stock market. According to data from Larry R Tabb of Bloomberg Intelligence (1) retail investors now account for 19.5% of order flow.

As the percentage of retail investors grow, understanding their actions becomes more and more profitable. If one can predict their actions or atleast understand how they work then this is very profitable. Such research is similar to what Engineers, Data Scientists and Researchers at Quant Firms like Renaissance Two Sigma do to create their investing models. Sucess in such research has netted funds like Rennisance's Medalion Fund a return of 66% annualized without fees over a 30 year lifespan whereas the S&P 500 , the most common US Stock Market Index has only returned 10%.

As can be seen by the chart above Robinhood is the second biggest choice of broker for retail investors. Until August 2020, Robinhood exported popularity data, which was captured and stored by the creators of RobinTrack. This dataset is a treasure trove because while it is easy to get information about trades in the market, it is hard to get data specifically about retail investors.